Bridging the Gap

Enhancing Financial Literacy for Autistic Adults

Background

Increased financial literacy, or the ability to earn, save, spend, and manage money, can impact the long-term economic outcomes of autistic people and their families. Financial literacy is something that isn’t taught but is increasingly becoming part of transition success plans. The motive behind this is simple: financial preparedness can lead to increased independence. Autistic people and their families can make informed financial decisions, leading to higher savings and resources. However, the disparity in financial education for autistic youth puts them at a significant disadvantage and inhibits their independence. Research suggests autistic youth understand the importance of financial capability and strive for financial independence, but lack the opportunity to learn skills and receive the support needed to achieve their financial goals.

Benefits of Financial Literacy

Being financially literate offers numerous benefits, empowering people to make informed decisions about their money and financial future. By understanding essential financial concepts such as budgeting, saving, and debt management, people can avoid common financial pitfalls, like accumulating unsustainable debt or falling prey to financial scams. Financial literacy also helps in preparing for emergencies and achieving long-term goals, such as buying a home or planning for retirement. With a solid foundation in financial literacy, people can approach financial decisions with greater confidence, ensuring a more financially secure future.

Key Points

- Disabled people are not often given the tools to manage their finances.

- This, in addition to systemic barriers (such as complex benefits systems, discrimination, etc.), puts disabled people at an increased risk of falling into poverty.

- Autistic adults recognize the importance of financial knowledge, but they often lack the material support to achieve their financial goals.

- Education on financial literacy, enhancing financial tools to be more accessible, and improving current financial policies are promising solutions to helping autistic people achieve greater financial indepen

The Issue

Despite its importance in society and its practical application in everyday life, financial education isn’t emphasized enough in the education system, resulting in many autistic youth and young adults lacking the financial knowledge needed for a successful life and independence. A study that investigated the financial literacy and behaviors of autistic adults compared to their non-autistic peers revealed that autistic adults demonstrated lower financial literacy, lacked confidence in financial knowledge, and struggled with daily financial management. They exhibited greater uncertainty about financial issues, reported higher anxiety related to financial matters, and were less likely to plan for long-term financial goals or emergencies.

Financial literacy is more than maintaining money and having independence. Without financial knowledge, individuals are at risk of poverty and limited economic mobility. Disabled people are two times as likely to face poverty as their peers without disabilities.

One reason for the lack of financial education may be the “Services Cliff” that autistic adults face once they finish high school or other secondary schooling. The “Services Cliff” refers to a consistent decrease in services and support offered to autistic adults following high school. Every type of service (for example, speech- language therapy, personal assistant services, social work, case management, etc.) decreases in amount between adolescence and adulthood. However, since autism is a lifelong condition, it’s reasonable to expect that many young people will continue to require some or even extensive services into adulthood.

Vocational and life skills services, like financial education, are particularly important to become employed, continue their education, or live more independently. All in all, the lack of financial literacy is especially troubling for autistic people as it is a pivotal component of improving their quality of life.

Financial Literacy is a Step Toward a Better Quality of Life

In our increasingly money-centered world, financial literacy is a crucial step toward a better quality of life, particularly for autistic adults, yet it is often overlooked. Early financial education can significantly benefit autistic children, preparing them to manage money effectively as adults. By equipping individuals with the necessary skills and support systems, financial literacy can offer a pathway to financial independence and empowerment, fostering confidence, self- esteem, and a sense of control over one’s financial future.

The goal of financial education is to empower individuals to take charge of their financial lives, enabling them to navigate the financial world with competence and achieve their goals through education, practice, and ongoing support. The lack of resources instantiates the need for policy solutions to address financial literacy challenges and make financial education more accessible for autistic adults.

Existing Solutions

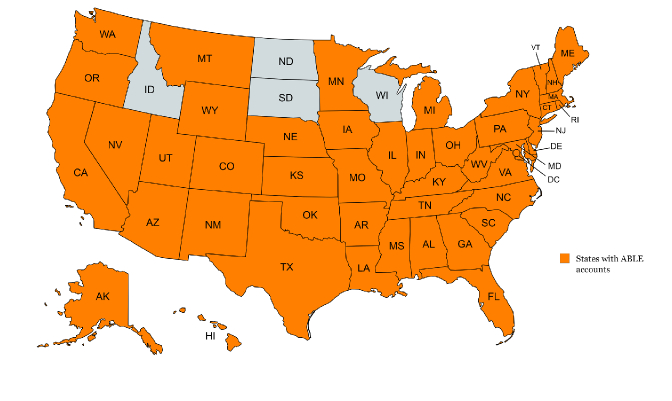

The following states (and D.C.) allow out-of-state participation for their ABLE accounts: Alabama, Alaska, Arkansas, California, Colorado, Connecticut, Delaware, Georgia, Hawaii, Illinois, Indiana, Iowa, Kansas, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Montana, Nebraska, Nevada, New Jersey, New York, North Carolina, Ohio, Oregon, Pennsylvania, Rhode Island, and Virginia. For more information about ABLE accounts in each state, and to use an interactive map, check out www.ablenrc.org.Map created with MapChart (www.mapchart.net).

The government has implemented policies to support disabled people financially. However, some of the provided benefits have major drawbacks:

- SSI: Established in 1973, the federal Supplemental Security Income (SSI) program offers monthly financial support to disabled or elderly individuals with minimal income and assets. However, the program has strict income and asset limits, and it reduces benefits for recipients with other income sources, or those living in Medicaid facilities or with supportive family members, making it difficult to save money for the future. Eligibility criteria are strict, and most SSI applications are initially rejected. Recent bipartisan efforts aim to relax these restrictions through the SSI Savings Penalty Elimination Act, which proposes higher asset limits to help recipients save for emergencies and retain Medicaid access. While this adjustment is crucial, broader updates to SSI are needed to improve financial security and reduce administrative strain.

- ABLE Accounts: These are tax-advantaged savings accounts for disabled individuals and their families, allowing income earned by the accounts to be tax-free. Contributions to the account, which can be made by any

person (the account beneficiary, family, friends, Special Needs Trust, or Pooled Trust), must be made using post-taxed dollars and are not tax deductible for federal taxes; however, some states may allow state income tax deductions for contributions made to an ABLE account. These accounts allow savings for disability-related expenses without affecting eligibility for SSI, Medicaid, and other means-tested programs. They supplement, but do not replace benefits from private insurance, Medicaid, SSI, and employment. While there are many benefits to these programs, these programs urgently need policy changes to improve the financial lives of recipients.

Policy Recommendations

Increase access to ATM and sensory-friendly banking options.

- In a study evaluating the financial capabilities of developmentally disabled people, it was discovered that they are more likely to prefer ATMs over online banking, showing their preference for a more hands-on approach to money handling. This easier way of monitoring spending proved to work well. However, a crucial disadvantage is that it is very easy to lose track of spending.

Include financial education as part of transition planning for autistic youth.

- Autistic participants in one study expressed a need for specialized financial education, emphasizing practical skills such as managing bills and taxes—simple skills that would greatly impact their future economic success and financial independence. These findings emphasize the need for enhanced collaboration between educational systems, caregivers, and financial institutions to provide comprehensive financial literacy programs for autistic youth.

Revise and modernize the SSI program to be more inclusive and beneficial to all disabled people.

- 4 in 10 applicants were found eligible for SSI between 2019 and 2021. Streamlining the SSI application process to reduce the high rejection rate would ensure that more disabled people receive the support they need.

- Modify the rules that reduce benefits for those with additional income sources, enabling recipients to achieve greater financial Implement policies that encourage long-term savings for SSI recipients, such as increasing the asset limits, to help people build a financial safety net for emergencies while retaining access to their benefits.

Written by: Isha Swaminathan

Edited by: The Policy Impact Project